Understanding Blockchain Transactions: A Beginner's Guide

Understanding blockchain transactions is crucial for anyone looking to delve into the world of cryptocurrencies and decentralized technologies. At its core, a blockchain transaction is a digital agreement that occurs over a blockchain network. Unlike traditional financial systems, where a centralized authority verifies transactions, blockchain relies on a decentralized network of computers (nodes) to confirm and record transactions. This method enhances security and transparency as each transaction is cryptographically signed and added to a public ledger.

To better understand how these transactions work, let's break it down into key components:

- Initiation: A user initiates a transaction, such as sending cryptocurrency to another user.

- Verification: The transaction is broadcasted to the network, where nodes validate it using complex algorithms.

- Inclusion: Once verified, the transaction is bundled with others into a block and added to the blockchain.

- Confirmation: The transaction is confirmed when the block is added to the chain, making it nearly impossible to alter.

Understanding these elements is the first step in grasping how blockchain technology is revolutionizing various industries.

Counter-Strike is a popular multiplayer first-person shooter game that has captivated gamers since its release. Players engage in team-based combat, where one side takes on the role of terrorists and the other as counter-terrorists. To enhance your gaming experience, don't forget to check out the bc.game promo code for exciting offers and bonuses.

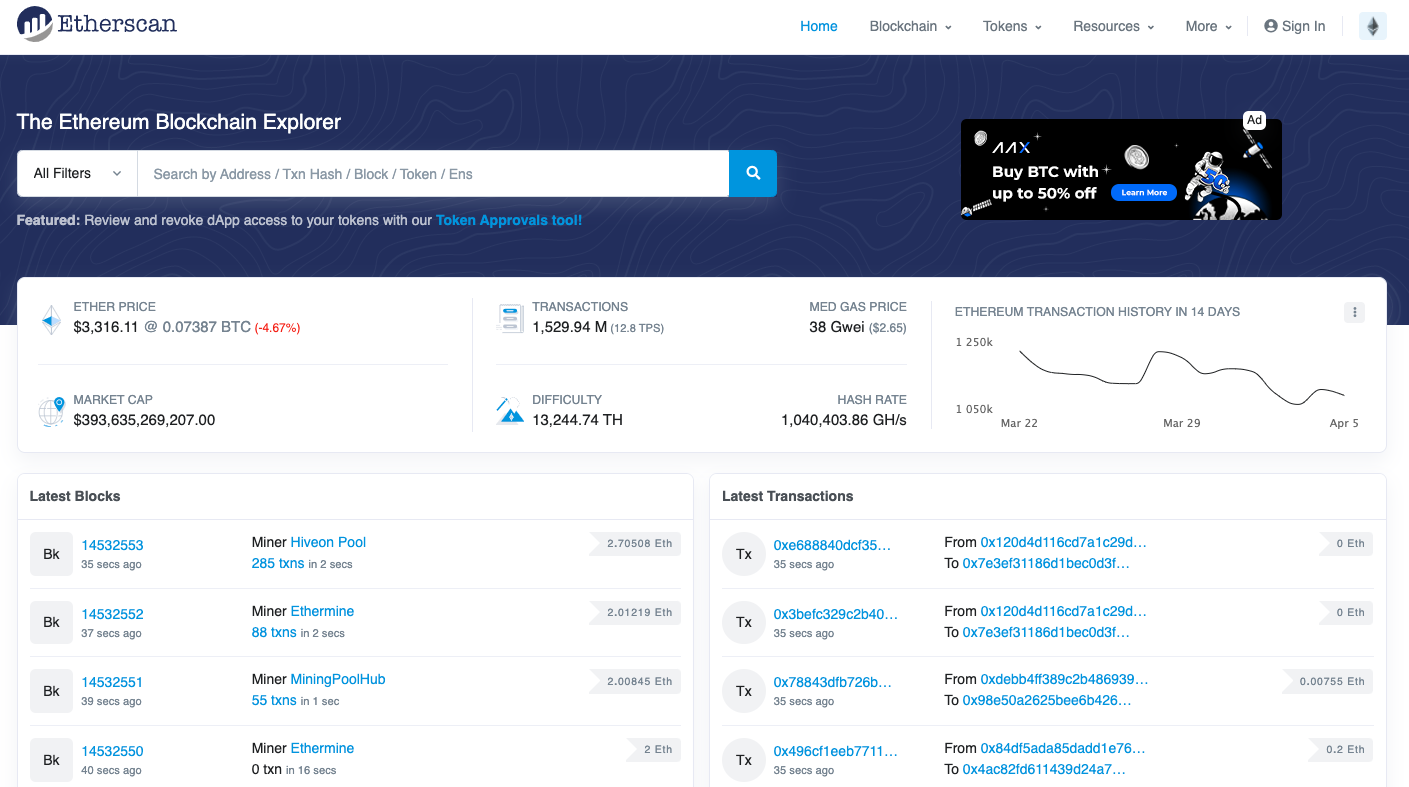

How to Trace Transactions on the Blockchain: Tools and Techniques

Tracing transactions on the blockchain is essential for understanding the flow of funds and ensuring transparency. There are several tools and techniques that can help you achieve this. One of the most popular tools is a blockchain explorer, which allows users to search for transaction details by entering a wallet address or transaction ID. These explorers present information such as transaction amounts, timestamps, and the addresses involved in the transaction, making it easier to track the movement of cryptocurrency.

Another technique to trace transactions is leveraging analytics platforms designed for in-depth blockchain analysis. These platforms often use algorithms to cluster addresses and identify patterns in transaction behavior. Some of the well-known blockchain analytics tools include Chainalysis and Elliptic, which can provide insights into suspicious activities and help businesses comply with regulations. Moreover, utilizing APIs offered by various service providers can automate the tracing process, allowing for real-time monitoring of transactions on the blockchain.

What Are Smart Contracts and How Do They Work on Blockchain?

Smart contracts are self-executing contracts with the terms of the agreement directly written into code. They reside on a blockchain, allowing for secure, transparent, and tamper-proof transactions without the need for intermediaries. By automating processes and reducing the risk of fraud, smart contracts can enhance efficiency in various industries, including finance, real estate, and healthcare. For example, a smart contract could automatically transfer ownership of a property once payment is confirmed, minimizing delays and potential disputes.

To understand how smart contracts work, it's essential to grasp the underlying technology: blockchain. A blockchain is a distributed ledger that records transactions across multiple computers, ensuring that the data is immutable and accessible to all parties involved. Smart contracts operate on platforms like Ethereum, where they are triggered by specific events, such as receiving digital currency. Once the conditions are met, the contract executes automatically, enforcing compliance without the need for human intervention. This self-sufficiency is what makes smart contracts a revolutionary component of blockchain technology.